- North American cannabis stocks have perhaps never been as cheap as they are today

Last week, The Seed Investor published an article on the current, “stupid-cheap” valuations for cannabis stocks. We pointed out that this extends to both Canadian- and U.S.-based companies.

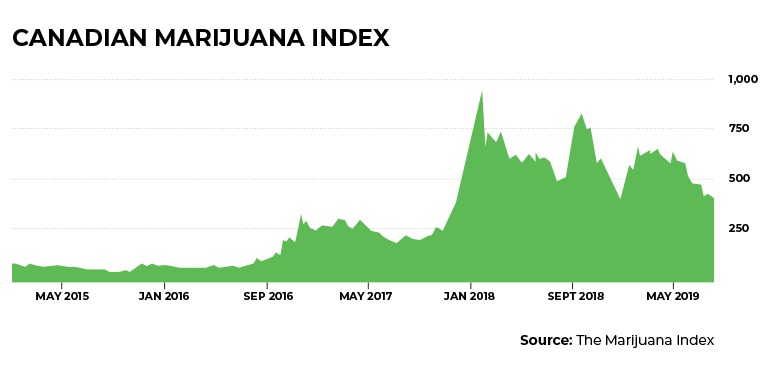

Sometimes a picture is worth a thousand words. In Canada, stocks currently languish in a deep trough.

Stocks are relatively cheaper now than when the entire industry went on a tear in 2017 when the entire sector more than quadrupled. Meanwhile, current fundamentals for the Canadian cannabis industry could not be more bullish.

- Three consecutive months of double-digit growth in cannabis retail sales

- Phase 2 of legalization (in October) will authorize value-added cannabis products, opening up new national markets for higher-margin edibles and concentrates

- Ontario, the one province that has slowed the growth of Canada’s cannabis industry the most, has just announced it will award 50 new retail licenses – more than tripling retail access to cannabis in the province

Strong revenue growth going forward for Canadian cannabis companies isn’t a possibility. It’s a certainty.

In the U.S., cannabis stocks are also trading at very steep discounts.

Additional states are legalizing cannabis. Congress is talking seriously about how to end federal Prohibition. Banking rules have been relaxed. The FDA has promised an improved regulatory structure for CBD products this fall. Multi-state operators continue to expand and deepen their cannabis operations.

None of this is being reflected in valuations for U.S. cannabis stocks.

Investors looking for bargains in the cannabis industry could practically pick their stocks blindfolded right now. But for cannabis investors seeking some specific names on which to do their due diligence, here are 8 candidates to consider – four in Canada and four in the U.S.

U.S. cannabis stocks:

Curaleaf Holdings (CAN:CURA / US:CURLF)

For investors looking for value in U.S.-based cannabis companies, why not start at the top? Curaleaf has made itself the world’s largest cannabis company (by revenues). Its recent acquisition of GR Companies (Grassroots) has cemented Curaleaf’s position. Its U.S. operational footprint is extensive:

- 131 dispensary licenses (68 locations operational)

- 20 cultivation sites

- 26 processing facilities

These operations now give Curaleaf access to a population base of 177 million people in the U.S. Yet with a market cap of $3.35 billion, Curaleaf is less than 1/3rd the size of Canada’s Big Dog, Canopy Growth (US: CGC / CAN: WEED): market cap $10.9 billion.

Obviously, Canopy Growth has some advantages over Curaleaf. This includes stronger listings, superior access to capital, and a strategic investor -- Constellation Brands (US:STZ) -- that has already injected billions in funding.

Put another way, these are areas where Curaleaf offers investors additional upside. It will obtain better listings (in the U.S. and Canada) as cannabis reform continues in the U.S. and Congress is now committed to ending Prohibition at the federal level.

It will get better access to banking services. Cannabis banking rules in the U.S. have already been relaxed. The Republican chair of the Senate Banking Committee, Mike Crapo, recently indicated support for reforming banking laws.

Curaleaf’s chart has gone roughly sideways over the past year since it obtained its public listing at the end of October 2018. This makes Curaleaf relatively one of the better performers among U.S. companies. Lots of upside potential here, and because of its size it will tend to benefit disproportionately as cannabis normalization continues in the U.S.

iAnthus Capital Holdings (CAN:IAN / US:ITHUF)

iAnthus certainly qualifies as a rival to Curaleaf as a major multi-state operator (MSO) in the U.S. While it has only 23 operational cannabis dispensaries today, with 68 total dispensary licenses its number of stores will increase rapidly. iAnthus’ cannabis products are now available in well over 100 dispensaries.

iAnthus generated $74 million in Q1 sales, but as noted that number is expected to rise substantially as more dispensaries are opened. Like Curaleaf, iAnthus is also committed to deep penetration of the market for CBD-based products. Here iAnthus already has CBD products placed in over 1100 stores, spanning 46 U.S. states. The FDA has signaled its intentions to bringing in new rules to facilitate CBD commerce this fall.

Then there is the value proposition.

While the operations and revenues of iAnthus have grown steadily, its market cap has been relentlessly shrinking. Indeed, with sentiment currently poor in the sector, valuations get steadily worse as we move to smaller companies. With a market cap of just $410 million, iAnthus offers investors big operations and big value.

Charlotte’s Web Holdings (CAN:CWEB / US:CWBHF)

Charlotte’s Web qualifies as Big Hemp in the United States. It currently has 862 acres of hemp under cultivation in 2019, after producing 675,000 lbs of hemp in 2018. Its hemp-based products are available in over 8,000 retail locations, making Charlotte’s Web the #1 CBD retailer. Revenues have risen by 74% year-over-year.

Taking some of the shine off of Charlotte’s Web as a value proposition today is that the company has been one of the few strong performers in the cannabis sector this summer. Its July 29, 2019 deal to get its CBD products into 1,350 Kroeger Stores is its single largest distribution deal to date. Favorable reaction to this has taken Charlotte Web’s market cap up to over $1 billion.

Since bottoming on June 14, 2019 at $11.06, the stock has been on a tear. Charlotte’s Web has more than doubled over that span to $23.74 (and is up over 10% today, as of this writing). Because of its dominance in U.S. CBD/hemp, Charlotte’s Web will be a big winner if the FDA crafts more industry-friendly rules for CBD this fall.

IONIC Brands (CAN:IONC / US:IONKF)

For the smaller U.S.-based companies, market caps aren’t merely compressed, they are absurd. IONIC Brands is a rising MSO. With a strong base in Washington State (including the leading vape brand), IONIC posted revenues of $7.5 million in 2018, representing a 3-year CAGR of 110%.

However, this year the Company obtained its public listing. With increased capitalization, IONIC has been acquiring additional premium brands. This includes Nevada’s leading vape (the “M” Stick) and a premium edibles line (Zoots), which are projected to add millions more to topline revenues this year.

An April 2019 deal with Origin House secures access for its products in over 500 California dispensaries. Then there is the value proposition.

The sour market conditions for cannabis stocks in 2019 have been punishing market caps right across the sector. IONIC has been hit especially hard since obtaining its listing in April, despite its solid revenue growth and a string of positive news announcements. After rising to as high as $0.90, IONIC is now trading at $0.13, representing a tiny market cap of $14.1 million – below its expected revenues for 2019.

The disconnect between price and value in U.S. cannabis stocks has arguably never been greater in the brief existence of this (now) legal industry. However, cannabis stock valuations in Canada are, if anything, even more absurd.

Canadian cannabis stocks:

HEXO Corp (CAN:HEXO / US:HEXO)

One of the larger Canadian cannabis companies, there are several reasons why investors may want to add HEXO to their portfolio. HEXO enjoys a dominant position in the Quebec cannabis industry, Canada’s second largest province, with over 1/3rd market share.

Its $1 billion cannabis distribution deal with Quebec’s provincial government is the single-largest distribution deal in the cannabis industry to date. Quebec’s government has signaled more restrictive regulations as Canada moves to Phase 2 of legalization, which will moderate HEXO’s opportunities for these new products.

However, HEXO has a major joint venture with Molson Coors Canada to enter the cannabis-infused beverage market. It already has a senior Canadian listing. It has upgraded its U.S. listing to the NYSE.

Despite these positives, HEXO sits with a market cap of just over $1 billion, having fallen by nearly half since it peaked at $8.28 on April 29, 2019. Shareholders should expect a significant revaluation simply from the upgraded NYSE listing alone. Strong value.

Valens GroWorks (CAN:VGW / US:VGWCF)

Regular readers of The Seed Investor know that we like Canadian cannabis extraction companies. Able to service Canada’s entire cannabis industry in providing critical cannabis oils, they can achieve (and have achieved) enormous scale.

Valens is the currently industry leader, with annual extraction capacity of 425,000 kilograms of dried cannabis. It’s in the process of expanding that capacity to 1 million kilograms per year. Valens is already profitable, having secured distribution deals with many of Canada’s industry leaders. With several different processes for oil extraction, Valens has the versatility (and scale) to meet the needs of the entire industry.

With other extraction contenders to choose from in Canada, what might set Valens apart at the moment is value. After peaking at $3.66 on May 16, 2019, Valens has given back roughly 30% of its market cap.

This erosion in price comes despite just reporting $8.8 million in Q2 revenue (a 296% increase over Q1) and Adjusted EBITDA of $2.0 million. Gross profit represented 58.0% of revenue. With strong margins, increasing scale, and more deals to come, there is every reason for investors to expect continued strong performance going forward.

Choom Holdings (CAN:CHOO / US:CHOOF)

As with U.S. cannabis companies, as soon as we shift our gaze to the smaller cannabis companies, we see even more compressed market caps – and stronger value propositions. As previously noted, Canada’s retail cannabis sector has finally caught fire. That surge in sales coincides exactly with Ontario (Canada’s largest province) finally getting in the game in opening up cannabis retail stores.

Choom is a play on Canadian cannabis retail, capitalizing on the disconnect as cannabis retail sales revenues soar while the market caps of Canadian cannabis retailers have continued to shrink.

As Ontario more-than-triples retail storefronts, the rapid growth in cannabis retail sales should not merely continue, it should accelerate. Choom already has a lucrative foothold in Ontario.

Canada’s cannabis retail leader, the province of Alberta, has announced it will be opening hundreds of new stores. Choom has one of the largest retail footprints in Alberta.

Phase 2 of cannabis legalization will open up new markets – for higher margin value-added products and Choom has just added a retail sector veteran with impressive credentials to leverage this growth potential. Opportunity knocks in Canadian cannabis retail.

MYM Nutraceuticals (CAN:MYM / US:MYMMF)

MYM Nutraceuticals offers cannabis investors both outstanding value and excellent revenue growth potential. As recent regulatory changes dramatically increased opportunities in hemp – in North America and around the world – the Company’s management team made the strategic decision to strongly pivot in that direction.

It’s paid off, from an operations standpoint. MYM’s focal point is its massive hemp farming operation in Saskatchewan (50% interest). The Company has 450 acres under hemp cultivation this year, estimating profits of CAD$13.9 million. This will jump to 3,000 acres for 2020 – with projected profits of CAD$70.8 million. A recent CAD$25 million sale accounts for half of MYM’s remaining biomass for sale this year.

Then there is the value.

(charts courtesy of Stockcharts.com)

After trading as high as $1.15 earlier this year, MYM is currently below $0.30, even after today’s gain of more than 10%. A market cap of a mere $35 million. That’s less than half of projected 2019 profits. It assigns no value to the Company’s U.S. hemp operations, Colombia operations, and additional operations in Canada. Outstanding value.

The absurd decline in cannabis valuations for most of 2019 has left cannabis investors hurting. The Canadian Marijuana Stock index has retreated back to December 2018 lows – despite Canadian cannabis retail catching fire. That’s more than just silly, that’s insane.

For investors, it’s a huge value opportunity.

DISCLOSURES: IONIC Brands, Choom Holdings, and MYM Nutraceuticals are clients of The Seed Investor. The writer also personally holds shares of Valens GroWorks.